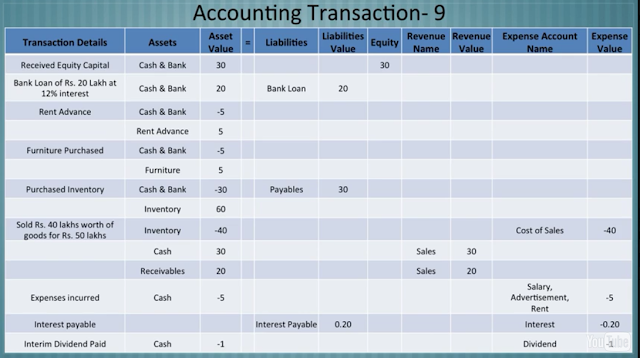

Learn how simple Balance Sheet Preparation is, you will easily understand logic behind this with this Image presentation posted below:

The Accounting Equation is a fundamental concept in accounting that represents the relationship between a company’s assets, liabilities, and equity. The equation is as follows:

Assets = Liabilities + Equity

The accounting equation must always be in balance, which means that the total assets of a company must equal the sum of its liabilities and equity. Every financial transaction affects the accounting equation, and it is important for accountants to understand how transactions affect each of the three components of the equation.

Let’s look at a few examples of transactions and how they affect the accounting equation:

- A company receives $10,000 cash from a customer for services rendered. This transaction increases the company’s cash account (an asset) by $10,000. Since there is no corresponding increase in liabilities or equity, the accounting equation becomes:

Assets = Liabilities + Equity $10,000 = 0 + $10,000

- The company purchases $5,000 worth of supplies on credit. This transaction increases the company’s supplies account (an asset) by $5,000, but it also increases the company’s accounts payable account (a liability) by $5,000 since the company has not yet paid for the supplies. The accounting equation becomes:

Assets = Liabilities + Equity $15,000 = $5,000 + $10,000

- The company pays $1,000 in cash for rent. This transaction decreases the company’s cash account (an asset) by $1,000, but it also decreases the company’s retained earnings (a component of equity) by $1,000 since the company’s net income is reduced by the rent expense. The accounting equation becomes:

Assets = Liabilities + Equity $14,000 = $5,000 + $9,000

In summary, every transaction in accounting affects the accounting equation by changing the values of assets, liabilities, and equity. It is essential for accountants to keep track of these changes to ensure that the accounting equation remains in balance.