Interview by Singhvi Online

Accounts Receivable interview questions by Singhvi Online

Category: Finance & Accounting

-

Accounts Payable Vs Accounts Receivable

AP and AR are both important accounting terms used to manage a company’s finances.

AP stands for Accounts Payable, which refers to the amount of money that a company owes to its vendors, suppliers, or other creditors for goods and services that have been received but not yet paid for. Essentially, it’s the amount that a company owes to others.

AR stands for Accounts Receivable, which refers to the amount of money that a company is owed by its customers for goods and services that have been sold but not yet paid for. Essentially, it’s the amount that others owe to the company.

Accounts Payable (AP) is a term used in accounting to refer to the amount of money that a company owes to its vendors or suppliers for goods or services that have been purchased but not yet paid for. AP is considered a liability on the company’s balance sheet.

When a company purchases goods or services on credit, it creates an accounts payable entry in its books. This entry records the amount owed to the vendor, the invoice date, the due date, and other details. Once the company pays the vendor, it records a corresponding entry in its books to reduce the AP balance and reflect the payment.

Managing AP involves processing invoices, reconciling statements, and making payments to vendors in a timely manner. Companies often have AP departments or personnel responsible for these tasks. Efficient AP management is important for maintaining good relationships with vendors and for ensuring that the company’s financial records are accurate and up-to-date.

Accounts Receivable (AR) refers to the money that a company is owed by its customers for goods or services that have been delivered or rendered but not yet paid for. It is an asset on the balance sheet of a company, representing the amount of money that is expected to be received in the future from its customers.

When a company sells its products or services on credit, it creates an account for each customer to whom it extends credit. The account is then recorded as an account receivable, indicating the amount owed by the customer to the company. The company keeps track of these accounts, and once the customer pays, the company records the transaction as a reduction in the accounts receivable balance and an increase in cash or another payment method.

Accounts Receivable are important for a company’s cash flow management, as they represent a significant portion of its current assets. Efficient management of accounts receivable is necessary to ensure that a company has enough cash to cover its operational expenses and to invest in its growth.

In other words, Accounts Payable is the money that a company needs to pay, and Accounts Receivable is the money that a company expects to receive. Managing both AP and AR effectively are crucial for a company’s financial health and cash flow management.

The AP (Accounts Payable) and AR (Accounts Receivable) processes are important financial processes in any organization. Here is a high-level overview of the typical flow of each process:

Accounts Payable (AP) Process Flow:

- Purchase Request: The process begins with a purchase request from a department within the organization.

- Purchase Order: The purchase request is reviewed and approved by the procurement department, which then issues a purchase order to the vendor.

- Invoice Receipt: Once the goods or services are received, the vendor issues an invoice to the organization.

- Invoice Verification: The invoice is verified against the purchase order and goods receipt to ensure accuracy.

- Approval: The invoice is then approved for payment by the appropriate department or individual within the organization.

- Payment: Payment is then made to the vendor according to the payment terms outlined in the contract.

- Recording: Finally, the payment is recorded in the organization’s accounting system.

Accounts Receivable (AR) Process Flow:

- Sales Order: The process begins with a sales order from a customer.

- Invoice Creation: An invoice is created based on the sales order and sent to the customer.

- Invoice Delivery: The invoice is delivered to the customer through various channels such as email or mail.

- Payment Receipt: The customer pays the invoice either through check, credit card or other payment options.

- Payment Verification: The payment received is verified against the invoice.

- Payment Recording: The payment is recorded in the organization’s accounting system.

- Follow-up: If payment is not received, follow-up is done with the customer to collect the payment.

Note that these are high-level overviews, and the details of the AP and AR processes can vary depending on the organization and the industry.

For Accounts Payable Interview Questions please check out below:

Accounts Payable Interview Q & A Session – Rohitashva Singhvi

For Accounts Receivable Interview Questions please check out below:

Accounts Receivable Interview Q & A Session – Rohitashva Singhvi

-

How to determine product costing for manufacturing company

Cost Components: Credit Google Product costing is a crucial aspect of managing a manufacturing concern, as it allows businesses to determine the total cost of producing a product. Knowing the total cost of production is important because it helps in setting a selling price that ensures profitability. In this blog, we will discuss how to do product costing for a manufacturing concern.

Step 1: Determine the direct material cost:

Direct material cost is the cost of raw materials that are used to produce a product. To determine the direct material cost, you need to identify the raw materials used in production and their cost per unit. Once you have identified the raw materials used, multiply the quantity of each material used by their respective cost per unit.

Direct material cost = Cost per unit of raw material X Quantity of raw material used

Material Cost: Credit Google -

Basics of General Accounting

Accounting is the process of recording, classifying, summarizing, and interpreting financial information. It is essential for businesses to keep track of their financial transactions and make informed decisions. The primary purpose of accounting is to provide financial information that is useful in making economic decisions.

Key Concepts

- Double-Entry System: Each transaction affects at least two accounts. The total debits must equal total credits.

- Accounting Equation: Assets = Liabilities + Equity. This fundamental equation must always be in balance.

- Financial Statements: The main financial statements are the Balance Sheet, Income Statement, Statement of Retained Earnings, and Cash Flow Statement.

- Accrual Accounting: Transactions are recorded when they are incurred, not necessarily when cash changes hands.

- GAAP and IFRS: Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) are the frameworks and guidelines for accounting.

Basic Journal Entries

Journal entries are the building blocks of accounting, recording the business transactions in the books.

Components of a Journal Entry

- Date: When the transaction occurred.

- Accounts: The accounts affected by the transaction.

- Debit and Credit: Amounts to be debited and credited.

- Description: A brief explanation of the transaction.

Common Journal Entries

- Initial Investment by Owners

- Debit: CashCredit: Owner’s Capital

Date Account Debit Credit ------------------------------------------------ YYYY-MM-DD Cash XXXX Owner's Capital XXXX - Purchase of Equipment for Cash

- Debit: EquipmentCredit: Cash

Date Account Debit Credit ------------------------------------------------ YYYY-MM-DD Equipment XXXX Cash XXXX - Purchase of Inventory on Credit

- Debit: InventoryCredit: Accounts Payable

Date Account Debit Credit ------------------------------------------------ YYYY-MM-DD Inventory XXXX Accounts Payable XXXX - Sales on Credit

- Debit: Accounts ReceivableCredit: Sales Revenue

Date Account Debit Credit ------------------------------------------------ YYYY-MM-DD Accounts Receivable XXXX Sales Revenue XXXX - Payment of Expenses (e.g., Rent)

- Debit: Rent ExpenseCredit: Cash

Date Account Debit Credit ------------------------------------------------ YYYY-MM-DD Rent Expense XXXX Cash XXXX

Advanced Journal Entries

As transactions become more complex, so do the journal entries.

- Depreciation of Equipment

- Debit: Depreciation ExpenseCredit: Accumulated Depreciation

Date Account Debit Credit ---------------------------------------------------- YYYY-MM-DD Depreciation Expense XXXX Accumulated Depreciation XXXX - Accrued Salaries (Salaries earned but not yet paid)

- Debit: Salaries ExpenseCredit: Salaries Payable

Date Account Debit Credit ---------------------------------------------------- YYYY-MM-DD Salaries Expense XXXX Salaries Payable XXXX - Prepaid Expenses (e.g., Prepaid Insurance)

- Initial Payment:

- Debit: Prepaid InsuranceCredit: Cash

Date Account Debit Credit ---------------------------------------------------- YYYY-MM-DD Prepaid Insurance XXXX Cash XXXX - At month-end adjustment:

- Debit: Insurance ExpenseCredit: Prepaid Insurance

Date Account Debit Credit ---------------------------------------------------- YYYY-MM-DD Insurance Expense XXXX Prepaid Insurance XXXX

- Initial Payment:

- Unearned Revenue (e.g., advance payment received for services to be provided later)

- When cash is received:

- Debit: CashCredit: Unearned Revenue

Date Account Debit Credit ---------------------------------------------------- YYYY-MM-DD Cash XXXX Unearned Revenue XXXX - When revenue is earned:

- Debit: Unearned RevenueCredit: Service Revenue

Date Account Debit Credit ---------------------------------------------------- YYYY-MM-DD Unearned Revenue XXXX Service Revenue XXXX

- When cash is received:

- Adjusting Entries for Bad Debts (Allowance Method)

- Estimate of bad debts:

- Debit: Bad Debt ExpenseCredit: Allowance for Doubtful Accounts

Date Account Debit Credit ---------------------------------------------------- YYYY-MM-DD Bad Debt Expense XXXX Allowance for Doubtful Accounts XXXX - Write-off of specific accounts:

- Debit: Allowance for Doubtful AccountsCredit: Accounts Receivable

Date Account Debit Credit ---------------------------------------------------- YYYY-MM-DD Allowance for Doubtful Accounts XXXXAccounts Receivable XXXX

- Estimate of bad debts:

Journal Entries for Provisions

1. Provision for Bad Debts

When estimating the provision:

- Debit: Bad Debt Expense

- Credit: Allowance for Doubtful Accounts

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Bad Debt Expense XXXX

Allowance for Doubtful Accounts XXXXWhen writing off specific bad debts:

- Debit: Allowance for Doubtful Accounts

- Credit: Accounts Receivable

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Allowance for Doubtful Accounts XXXX

Accounts Receivable XXXX2. Provision for Warranties

When creating the provision:

- Debit: Warranty Expense

- Credit: Provision for Warranties

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Warranty Expense XXXX

Provision for Warranties XXXXWhen actual warranty claims are made:

- Debit: Provision for Warranties

- Credit: Cash/Inventory (depending on how the warranty is settled)

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Warranties XXXX

Cash/Inventory XXXX3. Provision for Legal Claims

When estimating the provision:

- Debit: Legal Expense

- Credit: Provision for Legal Claims

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Legal Expense XXXX

Provision for Legal Claims XXXXWhen the legal claim is settled:

- Debit: Provision for Legal Claims

- Credit: Cash

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Legal Claims XXXX

Cash XXXXExample Scenario

Let’s consider an example where a company estimates a $5,000 warranty provision at year-end and incurs actual warranty costs of $2,000 the following year.

- Creating the provision at year-end:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-12-31 Warranty Expense 5,000

Provision for Warranties 5,000- Settling warranty claims the following year:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Warranties 2,000

Cash 2,000Provision Item Categories

Provisions are set aside for specific liabilities of uncertain timing or amount. They are recorded on both the income statement (as expenses) and the balance sheet (as liabilities). Understanding the categorization of provision items helps ensure accurate financial reporting.

Categories of Provisions

- Provision for Bad Debts (Allowance for Doubtful Accounts)

- Provision for Warranties

- Provision for Legal Claims

- Provision for Restructuring

- Provision for Environmental Liabilities

- Provision for Pension Liabilities

Journal Entries for Provision Items

1. Provision for Bad Debts

Income Statement (Expense):

- Bad Debt Expense

Balance Sheet (Liability):

- Allowance for Doubtful Accounts

Initial Entry:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Bad Debt Expense XXXX

Allowance for Doubtful Accounts XXXXWrite-off Specific Bad Debts:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Allowance for Doubtful Accounts XXXX

Accounts Receivable XXXX2. Provision for Warranties

Income Statement (Expense):

- Warranty Expense

Balance Sheet (Liability):

- Provision for Warranties

Initial Entry:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Warranty Expense XXXX

Provision for Warranties XXXXActual Warranty Claim Settlement:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Warranties XXXX

Cash/Inventory XXXX3. Provision for Legal Claims

Income Statement (Expense):

- Legal Expense

Balance Sheet (Liability):

- Provision for Legal Claims

Initial Entry:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Legal Expense XXXX

Provision for Legal Claims XXXXSettlement of Legal Claim:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Legal Claims XXXX

Cash XXXX4. Provision for Restructuring

Income Statement (Expense):

- Restructuring Expense

Balance Sheet (Liability):

- Provision for Restructuring

Initial Entry:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Restructuring Expense XXXX

Provision for Restructuring XXXXSettlement of Restructuring Costs:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Restructuring XXXX

Cash XXXX5. Provision for Environmental Liabilities

Income Statement (Expense):

- Environmental Expense

Balance Sheet (Liability):

- Provision for Environmental Liabilities

Initial Entry:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Environmental Expense XXXX

Provision for Environmental Liabilities XXXXSettlement of Environmental Liabilities:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Environmental Liabilities XXXX

Cash XXXX6. Provision for Pension Liabilities

Income Statement (Expense):

- Pension Expense

Balance Sheet (Liability):

- Provision for Pension Liabilities

Initial Entry:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Pension Expense XXXX

Provision for Pension Liabilities XXXXSettlement of Pension Liabilities:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Pension Liabilities XXXX

Cash XXXXReserves vs. Expenses

Reserves are generally created for expected future liabilities or losses and are considered part of equity. They are not expenses but are allocations of retained earnings to provide for future contingencies. Examples include:

- General Reserve

- Capital Reserve

Expenses are costs incurred during the operation of the business and directly impact the profit and loss statement. Provisions, when initially recorded, are treated as expenses. Examples include:

- Operating Expenses

- Administrative Expenses

- Financial Expenses

Legal Provisions and Dividends Categories

Legal provisions and dividends are essential aspects of accounting, representing potential future liabilities and distributions to shareholders, respectively. Let’s delve into the specifics of these categories and their journal entries.

1. Legal Provisions

Legal provisions are set aside for potential legal claims or lawsuits that may arise. These are recognized when it is probable that a liability has been incurred and the amount can be reasonably estimated.

Income Statement (Expense):

- Legal Expense

Balance Sheet (Liability):

- Provision for Legal Claims

Initial Entry to Record Provision:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Legal Expense XXXX

Provision for Legal Claims XXXXWhen the Legal Claim is Settled:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Provision for Legal Claims XXXX

Cash XXXXExample: Suppose a company estimates it will need $10,000 for a potential lawsuit.

Date Account Debit Credit

-----------------------------------------------------------

2024-06-01 Legal Expense 10,000

Provision for Legal Claims 10,000Later, if the lawsuit is settled for $8,000:

Date Account Debit Credit

-----------------------------------------------------------

2024-12-01 Provision for Legal Claims 8,000

Cash 8,0002. Dividends

Dividends are distributions of a company’s earnings to its shareholders. There are different types of dividends, including cash dividends and stock dividends.

Types of Dividends:

- Cash Dividends

- Stock Dividends

Income Statement:

- Dividends do not appear on the income statement as they are distributions of profit, not expenses.

Balance Sheet:

- When dividends are declared but not yet paid, they are recorded as a liability under Dividends Payable.

- Upon payment, this liability is reduced, and cash is decreased.

Declaration of Cash Dividends:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Retained Earnings XXXX

Dividends Payable XXXXPayment of Cash Dividends:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Dividends Payable XXXX

Cash XXXXExample: A company declares $5,000 in cash dividends to be paid at a later date.

Date Account Debit Credit

-----------------------------------------------------------

2024-06-01 Retained Earnings 5,000

Dividends Payable 5,000When the dividends are paid:

Date Account Debit Credit

-----------------------------------------------------------

2024-07-01 Dividends Payable 5,000

Cash 5,000Declaration of Stock Dividends: Stock dividends are distributed in the form of additional shares. The journal entry for stock dividends involves transferring the amount from Retained Earnings to Common Stock and Additional Paid-In Capital.

Declaration of Stock Dividends:

Date Account Debit Credit

-----------------------------------------------------------

YYYY-MM-DD Retained Earnings XXXX

Common Stock (at par value) XXXX

Additional Paid-In Capital XXXXExample: A company declares a 10% stock dividend on its $1 par value stock, with 1,000 shares outstanding. The market price is $10 per share.

Date Account Debit Credit

-----------------------------------------------------------

2024-06-01 Retained Earnings 1,000

Common Stock (at par value) 100

Additional Paid-In Capital 900Final Words

Mastering journal entries from basic to advanced levels is crucial for accurate financial reporting and analysis. By understanding these principles, you can ensure the integrity of your financial statements and maintain compliance with accounting standards.

Provisions are essential for recognizing potential future liabilities and ensuring that financial statements accurately reflect the company’s obligations. By properly accounting for provisions, businesses can better manage their financial health and comply with accounting standards.

Provisions are critical for ensuring that potential future liabilities are accounted for and that financial statements reflect a true and fair view of the company’s financial position. Properly categorizing and recording provisions help in maintaining the integrity of financial reporting.

Provisions are liabilities of uncertain timing or amount, often set aside for potential future obligations. Common examples include provisions for bad debts, warranties, or legal disputes. Creating journal entries for provisions typically involves recognizing the expense in the current period and creating a liability for the expected future payment.

Legal provisions and dividends require careful accounting treatment to ensure accurate financial reporting. Legal provisions are recognized as expenses when probable and measurable, while dividends are distributions from retained earnings. Understanding these categories and their journal entries helps maintain financial transparency and accountability.

-

How your Automobile or Vehicle Insurance Works?

Cars or any other Vehicle, but especially cars, are very expensive these days. For many people, buying a car takes years of hard work and a lot of savings. Therefore, it becomes crucial to ensure the safety of the vehicle through insurance Auto insurance is the best way to protect your car and the large sums of money invested in it Car insurance is basically an agreement between the insurance company and the car owner.

The latter is required to pay premiums for a certain fixed period, while the former undertakes to pay for any damage or loss to the vehicle In many countries, a car insurance policy is mandatory. Because this policy not only provides financial assistance to car owners but also greatly helps in the process of tracking vehicles such as theft.

Once you’ve decided which vehicle to buy, the most important thing you need to do is figure out how much liability coverage you need. For help and more information in this regard, you can consult your local car service. After determining the amount of liability, consider the type of coverage you want There are different types of car insurance policies available, and their coverage varies. For example, comprehensive auto insurance covers all accidents and vehicle theft. While fire and theft liability insurance only covers accidents where the insured’s vehicle collides with someone else’s vehicle. If another vehicle hits the insured, the company will not pay. It is up to you to decide which policy you accept. The cost of a policy varies mainly depending on the coverageTherefore, the more the policy covers, the higher its cost

Third, research the insurance company with which you want to purchase the policy you want. You can do this by checking the websites of various insurance agencies, getting completely free online quotes, conducting surveys in your social circles, and more. However, you should be aware that companies use statistical history to determine current exchange rates.

These rates depend on the funds needed to cover all claims and business expenses of the company. Auto insurance rates also depend on the insurance company you choose This is because each company offers a different claims experience and the number of people they insure varies. Also, the cost of doing business, the amount that must be paid to sell and service the policy, and the financial goals that must be achieved, vary from company to company.

The company will therefore charge accordingly In addition to this, there are several other factors that directly affect your car insurance rates These include your vehicle’s age, make and model, service usage, driving history, how you maintain your car, and your credit rating.

-

Advice on workers’ compensation claims

work accident

If you are involved in an accident at work, you must prove that your injury was caused by the negligence of the employer Your employer is also responsible for the actions of coworkers that cause the injury Remember that it is your responsibility to keep your employer informed of any accident that occurs while you are at work This information must be correctly recorded in the accident log. Note that your employer cannot terminate your employment if you file a compensation claim. If you have any questions or concerns about this, we recommend that you consult with us immediately

If you are an employer, self-employed person, or manager of a workplace, under the RIDDOR you must report certain types of work-related and work-related accidents, illnesses and hazardous occurrences

Reporting of accidents at work and occupational health problems is a legal requirement under the Reporting of Injuries, Illnesses and Hazardous Occurrences Regulations 1995 The information gathered helps local authorities and the Health and Safety Executive (HSE) to determine where and how the risks lie and to prevent their recurrence and further suffering and suffering for employees

You must declare all of the following:die

Seriously injured

Injured for more than three days (i.e. when the employee or self-employed person has an accident at work and cannot work for more than three days, but is not seriously injured);

work-related illnesses

dangerous event

The citizens were transported directly to the hospital

How soon should I report this incident? All reporting deadlines for work related injuries vary depending on severity and the following guidelines should be followed

If an accident results in death or serious injury to a person, we must be notified immediately.Injuries older than 3 days must be reported within 10 days

As soon as possible after a doctor diagnoses a work-related illness.

Hazardous occurrences must be reported immediately.Have you ever had an accident at work? If so, you will likely be able to file a claim with your employer’s insurance company An occupational injury can be defined as any workplace accident that could have been avoided If the accident at work is not your fault, you are entitled to reasonable financial compensation

Our lawyers are qualified members of the Law Society’s panel of personal injury specialists.

We provide free advice on workers’ compensation claims, including:Exposure to preventable health risks leading to workplace accidents

Lack of safety equipment leads to workplace accidents

Exposure to unnecessary hazards or health risks resulting in workplace accidents

A mechanical breakdown causes an accident at work

Poor maintenance of machines leads to work accidents

Unsafe working conditions that lead to workplace accidents

-

Simple Steps to learn Accounting for Balance Sheet Preparation

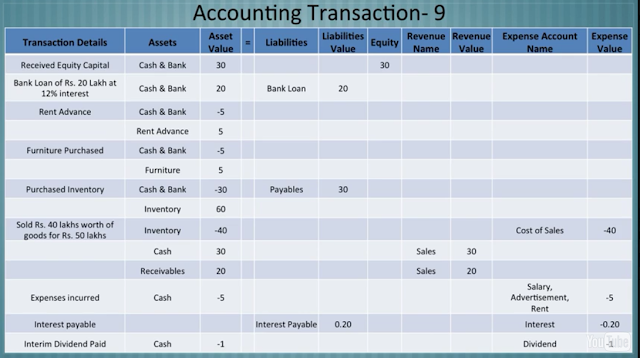

Learn how simple Balance Sheet Preparation is, you will easily understand logic behind this with this Image presentation posted below:

The Accounting Equation is a fundamental concept in accounting that represents the relationship between a company’s assets, liabilities, and equity. The equation is as follows:

Assets = Liabilities + Equity

The accounting equation must always be in balance, which means that the total assets of a company must equal the sum of its liabilities and equity. Every financial transaction affects the accounting equation, and it is important for accountants to understand how transactions affect each of the three components of the equation.

Let’s look at a few examples of transactions and how they affect the accounting equation:

- A company receives $10,000 cash from a customer for services rendered. This transaction increases the company’s cash account (an asset) by $10,000. Since there is no corresponding increase in liabilities or equity, the accounting equation becomes:

Assets = Liabilities + Equity $10,000 = 0 + $10,000

- The company purchases $5,000 worth of supplies on credit. This transaction increases the company’s supplies account (an asset) by $5,000, but it also increases the company’s accounts payable account (a liability) by $5,000 since the company has not yet paid for the supplies. The accounting equation becomes:

Assets = Liabilities + Equity $15,000 = $5,000 + $10,000

- The company pays $1,000 in cash for rent. This transaction decreases the company’s cash account (an asset) by $1,000, but it also decreases the company’s retained earnings (a component of equity) by $1,000 since the company’s net income is reduced by the rent expense. The accounting equation becomes:

Assets = Liabilities + Equity $14,000 = $5,000 + $9,000

In summary, every transaction in accounting affects the accounting equation by changing the values of assets, liabilities, and equity. It is essential for accountants to keep track of these changes to ensure that the accounting equation remains in balance.

Transaction Image to learn Accounting Transaction in more detail: Image for educational purpose only just used for Balance Sheet preparation -

Introduction – The Accounting Equation

From the large, multi-national corporation down to the corner beauty salon, every business transaction will have an effect on a company’s financial position. The financial position of a company is measured by the following items:

- Assets (what it owns)

- Liabilities (what it owes to others)

- Owner’s Equity (the difference between assets and liabilities)

The accounting equation (or basic accounting equation) offers us a simple way to understand how these three amounts relate to each other. The accounting equation for a sole proprietorship is:

The accounting equation for a corporation is:

Assets are a company’s resources—things the company owns. Examples of assets include cash, accounts receivable, inventory, prepaid insurance, investments, land, buildings, equipment, and goodwill. From the accounting equation, we see that the amount of assets must equal the combined amount of liabilities plus owner’s (or stockholders’) equity.Liabilities are a company’s obligations—amounts the company owes. Examples of liabilities include notes or loans payable, accounts payable, salaries and wages payable, interest payable, and income taxes payable (if the company is a regular corporation). Liabilities can be viewed in two ways:(1) as claims by creditors against the company’s assets, and

(2) a source—along with owner or stockholder equity—of the company’s assets.Owner’s equity or stockholders’ equity is the amount left over after liabilities are deducted from assets:Assets – Liabilities = Owner’s (or Stockholders’) Equity.Owner’s or stockholders’ equity also reports the amounts invested into the company by the owners plus the cumulative net income of the company that has not been withdrawn or distributed to the owners.If a company keeps accurate records, the accounting equation will always be “in balance,” meaning the left side should always equal the right side. The balance is maintained because every business transaction affects at least two of a company’s accounts. For example, when a company borrows money from a bank, the company’s assets will increase and its liabilities will increase by the same amount. When a company purchases inventory for cash, one asset will increase and one asset will decrease. Because there are two or more accounts affected by every transaction, the accounting system is referred to as double-entry accounting.A company keeps track of all of its transactions by recording them in accounts in the company’s general ledger.Each account in the general ledger is designated as to its type: asset, liability, owner’s equity, revenue, expense, gain, or loss account.We created a visual tutorial to demonstrate how a variety of transactions will affect the accounting equation and the financial statements. It is available in AccountingCoach PRO along with test questions that pertain to the accounting equation.Balance Sheet and Income Statement

The balance sheet is also known as the statement of financial position and it reflects the accounting equation. The balance sheet reports a company’s assets, liabilities, and owner’s (or stockholders’) equity at a specific point in time. Like the accounting equation, it shows that a company’s total amount of assets equals the total amount of liabilities plus owner’s (or stockholders’) equity.The income statement is the financial statement that reports a company’s revenues and expenses and the resulting net income. While the balance sheet is concerned with one point in time, the income statement covers a time interval or period of time. The income statement will explain part of the change in the owner’s or stockholders’ equity during the time interval between two balance sheets.

Thanks for Reading.

- New trends in accounting

- Effective Cost Control Strategies for Electrical Service Providers

- Effective Cost Control Strategies for Mechanical Service Providers

- 2025 IRS Tax Inflation Adjustments

- Rupee hits new low amid dollar strength

- The Intersection of Cinema and Business

- Property Loan in the UAE: Guide for 2024

- RERA: Dubai’s Pillar of Real Estate Security

- Personal Loan Process and Banks in the UAE

-

IFRS Standard & Interpretation Updates

Financial statement considerations in adopting new and revised pronouncements

Where new and revised pronouncements are applied for the first time, there can be consequential impacts on annual financial statements, including:

- Updates to accounting policies. The terminology and substance of disclosed accounting policies may need to be updated to reflect new recognition, measurement and other requirements, e.g. IAS 19 Employee Benefits may impact the measurement of certain employee benefits.

- Impact of transitional provisions. IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors contains a general requirement that changes in accounting policies are retrospectively applied, but this does not apply to the extent an individual pronouncement has specific transitional provisions.

- Disclosures about changes in accounting policies. Where an entity changes its accounting policy as a result of the initial application of an IFRS and it has an effect on the current period or any prior period, IAS 8 requires the disclosure of a number of matters, e.g. the title of the IFRS, the nature of the change in accounting policy, a description of the transitional provisions, and the amount of the adjustment for each financial statement line item affected

- Third statement of financial position. IAS 1 Presentation of Financial Statements requires the presentation of a third statement of financial position as at the beginning of the preceding period in addition to the minimum comparative financial statements in a number of situations, including if an entity applies an accounting policy retrospectively and the retrospective application has a material effect on the information in the statement of financial position at the beginning of the preceding period

- Earnings per share (EPS). Where applicable to the entity, IAS 33 Earnings Per Share requires basic and diluted EPS to be adjusted for the impacts of adjustments result from changes in accounting policies accounted for retrospectively and IAS 8requires the disclosure of the amount of any such adjustments.

Whilst disclosures associated with changes in accounting policies resulting from the initial application of new and revised pronouncements are less in interim financial reports under IAS 34 Interim Financial Reporting, some disclosures are required, e.g. description of the nature and effect of any change in accounting policies and methods of computation.

IFRS9 Financial Instruments (2014) {Effective for annual periods beginning on or after 1 January 2018}

A finalised version of IFRS 9 which contains accounting requirements for financial instruments, replacing IAS39 Financial Instruments: Recognition and Measurement. The standard contains requirements in the following areas:

For more information, read our previous post: Brief Overview of IFRS & How it’s different from US GAAP – Singhvi Online

Thanks for Reading.

- New trends in accounting

- Effective Cost Control Strategies for Electrical Service Providers

- Effective Cost Control Strategies for Mechanical Service Providers

- 2025 IRS Tax Inflation Adjustments

- Rupee hits new low amid dollar strength

- The Intersection of Cinema and Business

- Property Loan in the UAE: Guide for 2024

- RERA: Dubai’s Pillar of Real Estate Security

- Personal Loan Process and Banks in the UAE