Accountants often appreciate movies that engage with finance, present intricate puzzles, or simply bring satisfaction through the organization of ideas. Whether it’s exploring the complex world of high finance or watching underdog stories with a focus on strategy, these films offer a wide range of entertainment that accountants can enjoy. Here’s our curated list of 10 movies that might resonate with those in the accounting profession.

10 Must-See Movies for Accountants: A Curated List

1. The Wolf of Wall Street (2013)

Directed by Martin Scorsese, this biographical crime drama tells the story of Jordan Belfort, a stockbroker who built his career on fraud and corruption. It’s a rollercoaster ride through the excesses of Wall Street in the 80s and 90s, offering a thrilling look at the dark side of finance. Though not exactly a lesson in ethics, it’s a captivating depiction of high-stakes finance.

2. The Big Short (2015)

This film, based on Michael Lewis’s book, chronicles the events leading up to the 2008 financial crisis. It follows a group of investors who saw the housing market collapse coming and bet against it. The movie breaks down complex financial concepts in an entertaining way, providing a compelling narrative that’s both enlightening and engaging.

3. Moneyball (2011)

“Moneyball” is not about accounting in the traditional sense, but it explores the use of statistics and data analysis in sports. The story follows Billy Beane, the general manager of the Oakland Athletics, who uses a data-driven approach to build a competitive baseball team on a tight budget. It’s a perfect watch for those who appreciate numbers and the innovative application of analytics.

4. Glengarry Glen Ross (1992)

This drama, based on David Mamet’s play, dives into the cutthroat world of real estate sales. The intense performances and high-stakes scenarios showcase the pressure to perform and the ethical dilemmas that can arise in a sales-driven environment. While not about accounting, it offers insight into the challenges of a results-oriented profession.

5. The Accountant (2016)

In this action-thriller, Ben Affleck plays Christian Wolff, a mathematically gifted accountant with autism who secretly works for dangerous criminal organizations. The movie combines action with the analytical aspects of accounting, presenting a unique spin on the profession while highlighting the importance of accuracy and problem-solving.

6. Trading Places (1983)

This classic comedy features a social experiment involving a wealthy commodities trader and a streetwise hustler. The film explores the commodities trading world with a comedic twist, featuring Eddie Murphy and Dan Aykroyd in unforgettable roles. It’s a lighthearted exploration of finance with a comedic lens, offering laughs along with financial insights.

7. A Beautiful Mind (2001)

Though not directly about accounting, this biographical drama portrays the life of John Nash, a Nobel Prize-winning mathematician who battled schizophrenia. The film highlights the power of analytical thinking and problem-solving, themes that resonate with accountants who rely on their analytical skills to navigate complex financial scenarios.

8. The Shawshank Redemption (1994)

This film tells the story of Andy Dufresne, a man wrongfully convicted of murder and sentenced to life in prison. While it doesn’t focus on accounting, the themes of resilience and hope, along with Andy’s meticulous planning, might resonate with accountants who understand the value of patience and strategy in overcoming challenges.

9. Catch Me If You Can (2002)

Based on a true story, this film follows the exploits of Frank Abagnale Jr., a brilliant con artist who impersonated various professionals before turning 21. Though his methods are questionable, the film showcases the art of deception and the thrill of the chase, appealing to those who enjoy uncovering fraud and spotting financial inconsistencies.

10. The Matrix (1999)

While not about accounting or finance, “The Matrix” is a science fiction classic that explores the nature of reality and complex puzzles. It’s a thought-provoking film that challenges conventional thinking, making it appealing to analytical minds who enjoy piecing together clues and exploring deeper meanings.

Whether you’re looking for high-octane action or thoughtful drama, these films offer a variety of narratives that can appeal to accountants and finance professionals alike.

Enjoy your next movie night with this diverse selection!

In the realm of finance and accounting, the accrual basis stands as a cornerstone principle, guiding the recognition of revenue and expenditure. Unlike cash basis accounting, which records transactions when cash is exchanged, the accrual basis focuses on when revenue is earned or expenses are incurred, regardless of the timing of cash flows or invoice issuance. Let’s delve into this essential concept to grasp its significance in financial reporting.

Recognizing Revenue and Expenditure

Under the accrual basis of accounting, revenue and expenditure are acknowledged when they are earned or incurred, respectively. This means that transactions are recorded as they occur, reflecting the economic reality of business activities rather than the timing of cash movements.

For instance, imagine a scenario where a service provider delivers services to a customer, but payment is not received until a later date. Despite the delay in payment, revenue is recognized when the service is provided, aligning with the accrual basis principle.

Example 1: Revenue Recognition

Consider Company X, with a financial year ending on April 30. On April 5, 2025, Company X provides consulting services worth AED 12,000 to Customer A. Although the invoice is sent on May 10 and payment is received on June 15, revenue should be recognized on April 5, the date of service delivery. This ensures that revenue is recorded in the appropriate financial period, irrespective of invoice issuance or payment receipt.

Example 2: Expense Recognition

Continuing from the previous example, let’s examine expense recognition. Customer A, with a financial year also ending on April 30, incurs an expense when receiving services from Company X on April 5, 2025. Even if the invoice is received later or payment is made after the service, the expense should be recognized on April 5, aligning with the accrual basis principle.

The Significance

Embracing the accrual basis of accounting offers several advantages. Firstly, it provides a more accurate depiction of a company’s financial position by matching revenues with corresponding expenses, thus reflecting the true profitability of operations. Additionally, it enables better comparability across different accounting periods, facilitating informed decision-making for stakeholders.

In conclusion, understanding the accrual basis of accounting is paramount for businesses aiming to maintain transparency and accuracy in financial reporting. By recognizing revenue and expenditure when earned or incurred, rather than when cash transactions occur, companies can present a more comprehensive and reliable representation of their financial performance.

As we approach the dawn of a new accounting era, the International Financial Reporting Standards (IFRS) have undergone significant updates, ushering in changes that will reshape financial reporting for entities across the globe. Effective from 1 January 2024, these amendments aim to enhance transparency, address concerns raised by investors, and refine the accounting treatment for various transactions. In this blog post, we delve into the key amendments that entities need to be cognizant of in their financial reporting.

GX Year End Reminders

Paragraph 30 of IAS 8 mandates entities to disclose information about new accounting standards not yet effective, providing insights into the potential impact on their financial statements. Our summary encapsulates all new accounting standards and amendments issued up to 31 December 2023, applicable for accounting periods starting on or after 1 January 2024.

Amendment to IFRS 16 – Leases on Sale and Leaseback

The amendments to IFRS 16 introduce requirements addressing sale and leaseback transactions, specifically focusing on how entities should account for such transactions post the transaction date. Notably, sale and leaseback transactions featuring variable lease payments unrelated to an index or rate are likely to experience the most significant impact. For detailed guidance, refer to IFRS Manual of Accounting paragraph 15.155.1.

Published: September 2022

Effective Date: Annual periods beginning on or after 1 January 2024.

Amendment to IAS 1 – Non-current Liabilities with Covenants

These amendments to IAS 1 bring clarity to the impact of conditions that an entity must comply with within twelve months after the reporting period on the classification of a liability. The primary objective is to enhance the information provided by entities regarding liabilities subject to these conditions. Further insights can be found in In brief INT2022-16.

Published: January 2020 and November 2022

Effective Date: Annual periods beginning on or after 1 January 2024.

Amendment to IAS 7 and IFRS 7 – Supplier Finance

In response to investor concerns about the opacity of supplier finance arrangements, the amendments to IAS 7 and IFRS 7 mandate enhanced disclosures. These requirements aim to provide transparency on the effects of supplier finance arrangements on an entity’s liabilities, cash flows, and exposure to liquidity risk. For more details, refer to In brief INT2023-03.

Published: May 2023

Effective Date: Annual periods beginning on or after 1 January 2024 (with transitional reliefs in the first year).

Amendments to IAS 21 – Lack of Exchangeability

Entities with transactions or operations in a foreign currency that is not exchangeable at the measurement date for a specified purpose will be impacted by the amendments to IAS 21. Exchangeability is defined as the ability to obtain another currency with a normal administrative delay, and the transaction occurs through a market or exchange mechanism creating enforceable rights and obligations. Early adoption is available.

Published: August 2023

Effective Date: Annual periods beginning on or after 1 January 2025 (early adoption is available).

As entities gear up for the implementation of these new IFRS accounting standards, proactive measures and a thorough understanding of the amendments will be crucial. It is imperative for financial professionals and organizations to stay abreast of these changes, ensuring a seamless transition into the evolving landscape of international financial reporting. The effective management of these standards will not only ensure compliance but also contribute to the credibility and transparency of financial statements in an ever-changing economic environment.

In June 2023, the United Arab Emirates (UAE) witnessed a significant shift in its economic landscape with the introduction of the Corporate Tax. For businesses operating in the region, understanding and adhering to the associated guidelines became paramount. In this blog post, we’ll unravel the intricacies of these guidelines, providing businesses with a comprehensive roadmap to navigate the UAE’s tax framework.

Calculate Taxable Income:

The journey begins with calculating your company’s taxable income—a fundamental step in the tax process. Businesses must meticulously determine their profits after factoring in allowable deductions and expenses. The guidelines offer clarity on which expenses are deductible and provide insights into handling unique situations, such as foreign income and free zone operations.

Apply the Tax Rate:

Once your taxable income is established, the next step is applying the tax rate. The standard corporate tax rate in the UAE stands at 9%. However, exemptions and reduced rates are applicable to certain entities. Understanding this is crucial, as it determines the percentage of your taxable income that will be allocated to tax obligations.

Convert Foreign Currency Transactions:

Operating in a global economy often involves dealing with multiple currencies. For tax purposes, the UAE dirham (AED) is the official currency, necessitating the conversion of foreign transactions into AED. This involves utilizing exchange rates set by the authorities to translate the value of income earned in other currencies into AED for accurate tax calculations.

Comply with Reporting and Payment Requirements:

Fulfilling reporting and payment obligations marks the final leg of this journey. The guidelines meticulously outline deadlines and procedures for electronically filing tax returns and making timely tax payments. Compliance at this stage ensures businesses meet their tax obligations accurately and within the stipulated time frames.

Additional Considerations:

Given the novelty of these guidelines, businesses should remain vigilant for any further clarifications or updates from the authorities. Staying informed is key, and consulting with qualified tax professionals is strongly advised to ensure continued compliance with the evolving tax landscape.

Remember:

It’s important to note that this information serves as a general guide and does not constitute financial or tax advice. Businesses are encouraged to seek professional guidance to address their specific circumstances and ensure compliance with the UAE Corporate Tax & Currency Conversion Guidelines.

Conclusion:

In conclusion, these guidelines serve as a compass for businesses navigating the complex terrain of the UAE Corporate Tax. By understanding and implementing these steps, companies can not only meet their tax obligations but also contribute to the economic stability and growth of the UAE. Stay informed, seek professional advice, and embark on this journey with confidence and compliance.

Broadly, Corporate Tax applies to the following “Taxable Persons”:

UAE companies and other juridical persons that are incorporated or effectively managed and controlled in the UAE;

Natural persons (individuals) who conduct a Business or Business Activity in the UAE as specified in a Cabinet Decision to be issued in due course; and

Non-resident juridical persons (foreign legal entities) that have a Permanent Establishment in the UAE (which is explained under [Section 8]).

Juridical persons established in a UAE Free Zone are also within the scope of Corporate Tax as “Taxable Persons” and will need to comply with the requirements set out in the Corporate Tax Law. However, a Free Zone Person that meets the conditions to be considered a Qualifying Free Zone Person can benefit from a Corporate Tax rate of 0% on their Qualifying Income (the conditions are included in [Section 14]).

Non-resident persons that do not have a Permanent Establishment in the UAE or that earn UAE sourced income that is not related to their Permanent Establishment may be subject to Withholding Tax (at the rate of 0%). Withholding tax is a form of Corporate Tax collected at source by the payer on behalf of the recipient of the income. Withholding taxes exist in many tax systems and typically apply to the cross-border payment of dividends, interest, royalties and other types of income.

Certain types of businesses or organisations are exempt from Corporate Tax given their importance and contribution to the social fabric and economy of the UAE. These are known as Exempt Persons and include:

Automatically exempt

● Government Entities● Government Controlled Entities that are specified in a Cabinet Decision

Exempt if notified to the Ministry of Finance (and subject to meeting certain conditions)

Exempt if applied to and approved by the Federal Tax Authority (and subject to meeting certain conditions)

● Public or private pension and social security funds● Qualifying Investment Funds● Wholly-owned and controlled UAE subsidiaries of a Government Entity, a Government Controlled Entity, a Qualifying Investment Fund, or a public or private pension or social security fund

In addition to not being subject to Corporate Tax, Government Entities, Government Controlled Entities that are specified in a Cabinet Decision, Extractive Businesses and Non-Extractive Natural Resource Businesses may also be exempted from any registration, filing and other compliance obligations imposed by the Corporate Tax Law, unless they engage in an activity which is within the charge of Corporate Tax.

In line with the tax regimes of most countries, the Corporate Tax Law taxes income on both a residence and source basis. The applicable basis of taxation depends on the classification of the Taxable Person.

A “Resident Person” is taxed on income derived from both domestic and foreign sources (i.e. a residence basis).

A “Non-Resident Person” will be taxed only on income derived from sources within the UAE (i.e. a source basis).

Residence for Corporate Tax purposes is not determined by where a person resides or is domiciled but instead by specific factors that are set out in the Corporate Tax Law. If a Person does not satisfy the conditions for being either a Resident or a Non-Resident person then they will not be a Taxable Person and will not therefore be subject to Corporate Tax.

Companies and other juridical persons that are incorporated or otherwise formed or recognised under the laws of the UAE will automatically be considered a Resident Person for Corporate Tax purposes. This covers juridical persons incorporated in the UAE under either mainland legislation or applicable Free Zone regulations, and would also include juridical persons created by a specific statute (e.g. by a special decree).

Foreign companies and other juridical persons may also be treated as Resident Persons for Corporate Tax purposes where they are effectively managed and controlled in the UAE. This shall be determined with regard to the specific circumstances of the entity and its activities, with a determining factor being where key management and commercial decisions are in substance made.

Natural persons will be subject to Corporate Tax as a “Resident Person” on income from both domestic and foreign sources, but only insofar as such income is derived from a Business or Business Activity conducted by the natural person in the UAE. Any other income earned by a natural person would not be within the scope of Corporate Tax.

Non-Resident Persons are juridical persons who are not Resident Persons and:

have a Permanent Establishment in the UAE; or

derive State Sourced Income.

Non-Resident Persons will be subject to Corporate Tax on Taxable Income that is attributable to their Permanent Establishment (which is explained under Section 8).

Certain UAE sourced income of a Non-Resident Person that is not attributable to a Permanent Establishment in the UAE will be subject to Withholding Tax at the rate of 0%.

The concept of Permanent Establishment is an important principle of international tax law used in corporate tax regimes across the world. The main purpose of the Permanent Establishment concept in the UAE Corporate Tax Law is to determine if and when a foreign person has established sufficient presence in the UAE to warrant the business profits of that foreign person to be subject to Corporate Tax.

The definition of Permanent Establishment in the Corporate Tax Law has been designed on the basis of the definition provided in Article 5 of the OECD Model Tax Convention on Income and Capital and the position adopted by the UAE under the Multilateral Instrument to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting. This allows foreign persons to use the relevant Commentary of Article 5 of the OECD Model Tax Convention when assessing whether they have a Permanent Establishment or not in the UAE. This assessment should consider the provisions of any bilateral tax agreement between the country of residence of the Non-Resident Person and the UAE.

Corporate Tax is imposed on Taxable Income earned by a Taxable Person in a Tax Period.

Corporate Tax would generally be imposed annually, with the Corporate Tax liability calculated by the Taxable Person on a self-assessment basis. This means that the calculation and payment of Corporate Tax is done through the filing of a Corporate Tax Return with the Federal Tax Authority by the Taxable Person.

The starting point for calculating Taxable Income is the Taxable Person’s accounting income (i.e. net profit or loss before tax) as per their financial statements. The Taxable Person will then need to make certain adjustments to determine their Taxable Income for the relevant Tax Period. For example, adjustments to accounting income may need to be made for income that is exempt from Corporate Tax and for expenditure that is wholly or partially non-deductible for Corporate Tax purposes.

The Corporate Tax Law also exempts certain types of income from Corporate Tax. This means that a Taxable Persons will not be subject to Corporate Tax on such income and cannot claim a deduction for any related expenditure. Taxable Persons who earn exempt income will remain subject to Corporate Tax on their Taxable Income.

The main purpose of certain income being exempt from Corporate Tax is to prevent double taxation on certain types of income. Specifically, dividends and capital gains earned from domestic and foreign shareholdings will generally be exempt from Corporate Tax. Furthermore, a Resident Person can elect, subject to certain conditions, to not take into account income from a foreign Permanent Establishment for UAE Corporate Tax purposes.

In principle, all legitimate business expenses incurred wholly and exclusively for the purposes of deriving Taxable Income will be deductible, although the timing of the deduction may vary for different types of expenses and the accounting method applied. For capital assets, expenditure would generally be recognised by way of depreciation or amortisation deductions over the economic life of the asset or benefit.

Expenditure that has a dual purpose, such as expenses incurred for both personal and business purposes, will need to be apportioned with the relevant portion of the expenditure treated as deductible if incurred wholly and exclusively for the purpose of the taxable person’s business.

Certain expenses which are deductible under general accounting rules may not be fully deductible for Corporate Tax purposes. These will need to be added back to the Accounting Income for the purposes of determining the Taxable Income. Examples of expenditure that is or may not be deductible (partially or in full) include:

Types of Expenditures

Limitation to deductibility

BribesFines and penalties (other than amounts awarded as compensation for damages or breach of contract)Donations, grants or gifts made to an entity that is not a Qualifying Public Benefit EntityDividends and other profits distributionsCorporate Tax imposed under the Corporate Tax LawExpenditure not incurred wholly and exclusively for the purposes of the Taxable person’s BusinessExpenditure incurred in deriving income that is exempt from Corporate Tax

No deduction

Client entertainment expenditure

Partial deduction of 50% of the amount of the expenditure

Interest expenditure

Deduction of net interest expenditure exceeding a certain de minimis thresholdup to 30% of the amount of earnings before the deduction of interest, tax, depreciation and amortisation (except for certain activities)

Corporate Tax will be levied at a headline rate of 9% on Taxable Income exceeding AED 375,000. Taxable Income below this threshold will be subject to a 0% rate of Corporate Tax.

Corporate Tax will be charged on Taxable Income as follows:

Resident Taxable Persons

Taxable Income not exceeding AED 375,000(this amount is to be confirmed in a Cabinet Decision)

0%

Taxable Income exceeding AED 375,000

9%

Qualifying Free Zone Persons

Qualifying Income

0%

Taxable Income that does not meet the Qualifying Income definition

A 0% withholding tax may apply to certain types of UAE sourced income paid to non-residents. Because of the 0% rate, in practice, no withholding tax would be due and there will be no withholding tax related registration and filing obligations for UAE businesses or foreign recipients of UAE sourced income.

Withholding tax does not apply to transactions between UAE resident persons.

A Free Zone Person that is a Qualifying Free Zone Person can benefit from a preferential Corporate Tax rate of 0% on their “Qualifying Income” only.

In order to be considered a Qualifying Free Zone Person, the Free Zone Person must:

maintain adequate substance in the UAE;

derive ‘Qualifying Income’;

not have made an election to be subject to Corporate Tax at the standard rates; and

comply with the transfer pricing requirements under the Corporate Tax Law.

The Minister may prescribe additional conditions that a Qualifying Free Zone Person must meet.

If a Qualifying Free Zone Person fails to meet any of the conditions, or makes an election to be subject to the regular Corporate Tax regime, they will be subject to the standard rates of Corporate Tax from the beginning of the Tax Period where they failed to meet the conditions.

Two or more Taxable Persons who meet certain conditions (see below) can apply to form a “Tax Group” and be treated as a single Taxable Person for Corporate Tax purposes.

To form a Tax Group, both the parent company and its subsidiaries must be resident juridical persons, have the same Financial Year and prepare their financial statements using the same accounting standards.

Additionally, to form a Tax Group, the parent company must:

own at least 95% of the share capital of the subsidiary;

hold at least 95% of the voting rights in the subsidiary; and

is entitled to at least 95% of the subsidiary’s profits and net assets.

The ownership, rights and entitlement can be held either directly or indirectly through subsidiaries, but a Tax Group cannot include an Exempt Person or Qualifying Free Zone Person.

To determine the Taxable Income of a Tax Group, the parent company must prepare consolidated financial accounts covering each subsidiary that is a member of the Tax Group for the relevant Tax Period. Transactions between the parent company and each group member and transactions between the group members would be eliminated for the purposes of calculating the Taxable Income of the Tax Group.

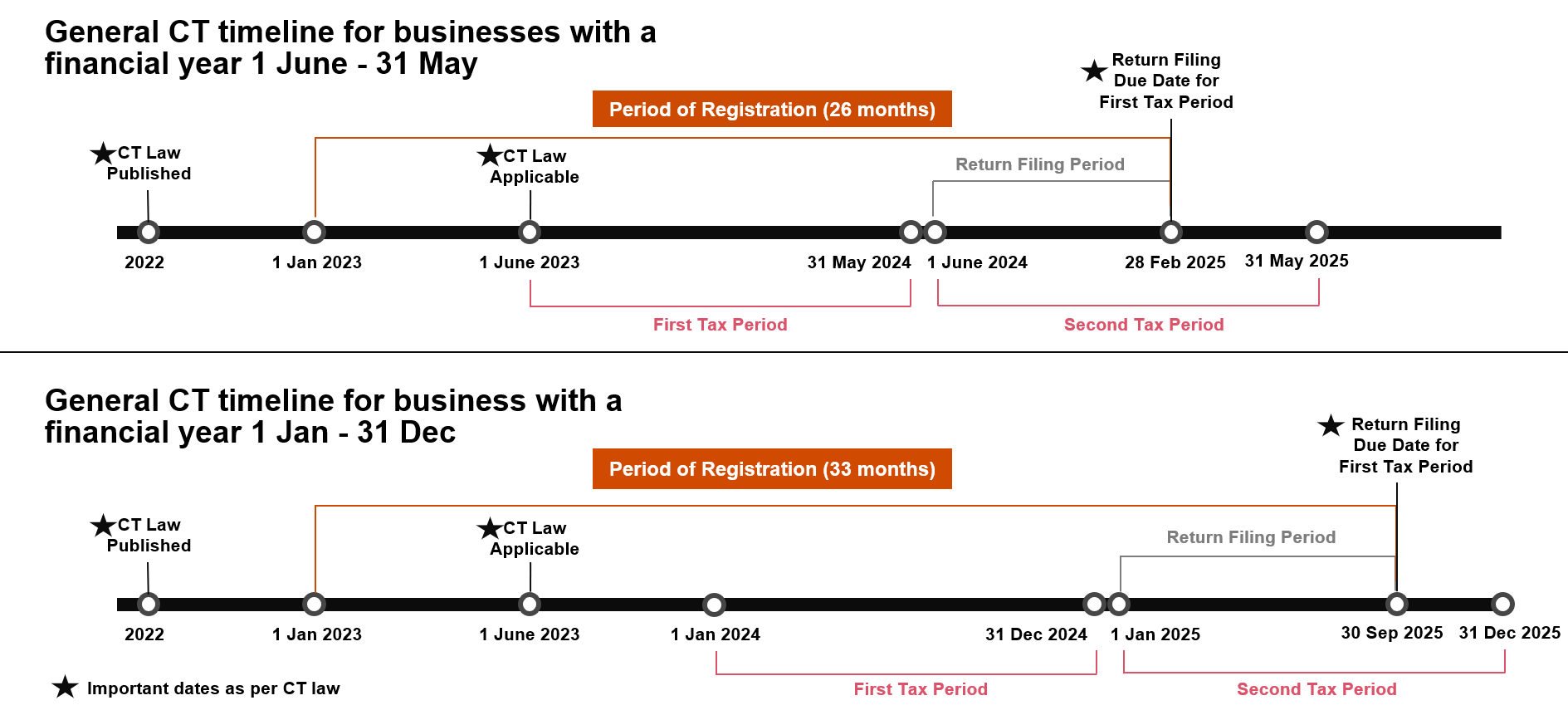

All Taxable Persons (including Free Zone Persons) will be required to register for Corporate Tax and obtain a Corporate Tax Registration Number. The Federal Tax Authority may also request certain Exempt Persons to register for Corporate Tax.

Taxable Persons are required to file a Corporate Tax return for each Tax Period within 9 months from the end of the relevant period. The same deadline would generally apply for the payment of any Corporate Tax due in respect of the Tax Period for which a return is filed.

Illustrated below are examples of the registration, filing and payment deadlines associated for Taxable Persons with a Tax Period (Financial Year) ending on 31 May or 31 December (respectively).

Read the Corporate Tax Law and the supporting information available on the websites of the Ministry of Finance and the Federal Tax Authority.

Use the available information to determine whether your business will be subject to Corporate Tax and if so, from what date.

Understand the requirements for your business under the Corporate Tax Law, including, for example:

Whether and by when your business needs to register for Corporate Tax;

What is the accounting / Tax Period for your business;

By when your business would need to file a Corporate Tax return;

What elections or applications your business may or should make for Corporate Tax purposes;

What financial information and records your business will need to keep for Corporate Tax purposes;

Regularly check the websites of the Ministry of Finance and the Federal Tax Authority for further information and guidance on the Corporate Tax regime.

Sources: FTA

RSS Error: https://wealthcreatorhub.in/feed/ is invalid XML, likely due to invalid characters. XML error: Reserved XML Name at line 2, column 39

The “spell number” function is a tool used by accountants and finance professionals to convert numerical values into their written word form. This function is typically used to generate the written representation of a specific amount or value, such as converting “1234.56” to “one thousand two hundred thirty-four and 56/100 dollars.”

The spell number function can be beneficial in various accounting and financial scenarios, including:

Writing checks: When preparing checks, it is customary to write out the amount in words to minimize the risk of alteration or fraud. The spell number function allows accountants to automatically generate the written form of the check amount.

Financial reports: In financial reports, especially those prepared for presentation or legal purposes, it can be useful to provide both the numerical value and the written form of amounts. The spell number function assists in generating the written representation of numbers, enhancing the clarity and comprehensibility of financial statements.

Invoicing and billing: Some organizations or industries may require invoices or billing statements to include the written form of the invoiced amounts. The spell number function helps automate this process, ensuring accuracy and consistency in the presentation of financial information.

Compliance and regulatory requirements: Certain regulations or jurisdictions might mandate the inclusion of written amounts in specific financial documents. The spell number function can facilitate compliance with these requirements, reducing the risk of non-compliance or errors.

Presentations and proposals: When delivering financial presentations or proposals, using the written form of amounts can enhance professionalism and improve the audience’s understanding. The spell number function allows accountants to quickly convert numerical data into a more easily digestible format.

It’s worth noting that the specific implementation and availability of a spell number function may vary depending on the accounting software, spreadsheet application, or programming language being used.

To update the code in your Excel workbook, follow these steps:

Open your Excel workbook.

Press Alt + F11 to open the VBA Editor.

In the VBA Editor, find the module where the code is currently located. It may have the same name as the worksheet containing the cell you want to use the spell-in-numbers function.

Double-click on the module to open it.

Replace the existing code with the updated code you received earlier.

Save the workbook by pressing Ctrl + S or by clicking on the save button.

Close the VBA Editor by clicking the close button (X) or by pressing Alt + Q.

Now you can use the SpellNumber function in your Excel worksheet.

In a cell where you want to display the spell-in-numbers conversion, enter the following formula: =SpellNumber(A1) (assuming the number you want to convert is in cell A1).

Press Enter to see the converted number in words.

Make sure to replace A1 with the cell reference that contains the number you want to convert.

That’s it! The code is now updated in your Excel workbook, and you can use the SpellNumber function to convert numbers to words.

Below codes (USD & Dirham) for your use(enjoy the benefits)

Option Explicit

'Main Function

Function SpellNumber(ByVal MyNumber)

Dim Dollars, Cents, Temp

Dim DecimalPlace, Count

ReDim Place(9) As String

Place(2) = " Thousand "

Place(3) = " Million "

Place(4) = " Billion "

Place(5) = " Trillion "

' String representation of amount.

MyNumber = Trim(Str(MyNumber))

' Position of decimal place 0 if none.

DecimalPlace = InStr(MyNumber, ".")

' Convert cents and set MyNumber to dollar amount.

If DecimalPlace > 0 Then

Cents = GetTens(Left(Mid(MyNumber, DecimalPlace + 1) & "00", 2))

MyNumber = Trim(Left(MyNumber, DecimalPlace - 1))

End If

Count = 1

Do While MyNumber <> ""

Temp = GetHundreds(Right(MyNumber, 3))

If Temp <> "" Then Dollars = Temp & Place(Count) & Dollars

If Len(MyNumber) > 3 Then

MyNumber = Left(MyNumber, Len(MyNumber) - 3)

Else

MyNumber = ""

End If

Count = Count + 1

Loop

Select Case Dollars

Case ""

Dollars = "No Dollars"

Case "One"

Dollars = "One Dollar"

Case Else

Dollars = Dollars & " Dollars"

End Select

Select Case Cents

Case ""

Cents = " and No Cents"

Case "One"

Cents = " and One Cent"

Case Else

Cents = " and " & Cents & " Cents"

End Select

SpellNumber = Dollars & Cents

End Function

' Converts a number from 100-999 into text

Function GetHundreds(ByVal MyNumber)

Dim Result As String

If Val(MyNumber) = 0 Then Exit Function

MyNumber = Right("000" & MyNumber, 3)

' Convert the hundreds place.

If Mid(MyNumber, 1, 1) <> "0" Then

Result = GetDigit(Mid(MyNumber, 1, 1)) & " Hundred "

End If

' Convert the tens and ones place.

If Mid(MyNumber, 2, 1) <> "0" Then

Result = Result & GetTens(Mid(MyNumber, 2))

Else

Result = Result & GetDigit(Mid(MyNumber, 3))

End If

GetHundreds = Result

End Function

' Converts a number from 10 to 99 into text.

Function GetTens(TensText)

Dim Result As String

Result = "" ' Null out the temporary function value.

If Val(Left(TensText, 1)) = 1 Then ' If value between 10-19...

Select Case Val(TensText)

Case 10: Result = "Ten"

Case 11: Result = "Eleven"

Case 12: Result = "Twelve"

Case 13: Result = "Thirteen"

Case 14: Result = "Fourteen"

Case 15: Result = "Fifteen"

Case 16: Result = "Sixteen"

Case 17: Result = "Seventeen"

Case 18: Result = "Eighteen"

Case 19: Result = "Nineteen"

Case Else

End Select

Else ' If value between 20-99...

Select Case Val(Left(TensText, 1))

Case 2: Result = "Twenty "

Case 3: Result = "Thirty "

Case 4: Result = "Forty "

Case 5: Result = "Fifty "

Case 6: Result = "Sixty "

Case 7: Result = "Seventy "

Case 8: Result = "Eighty "

Case 9: Result = "Ninety "

Case Else

End Select

Result = Result & GetDigit(Right(TensText, 1)) ' Retrieve ones place.

End If

GetTens = Result

End Function

' Converts a number from 1 to 9 into text.

Function GetDigit(Digit)

Select Case Val(Digit)

Case 1: GetDigit = "One"

Case 2: GetDigit = "Two"

Case 3: GetDigit = "Three"

Case 4: GetDigit = "Four"

Case 5: GetDigit = "Five"

Case 6: GetDigit = "Six"

Case 7: GetDigit = "Seven"

Case 8: GetDigit = "Eight"

Case 9: GetDigit = "Nine"

Case Else: GetDigit = ""

End Select

End Function

Option Explicit

'Main Function

Function SpellNumber(ByVal MyNumber)

Dim Dirhams, Fils, Temp

Dim DecimalPlace, Count

ReDim Place(9) As String

Place(2) = " Thousand "

Place(3) = " Million "

Place(4) = " Billion "

Place(5) = " Trillion "

' String representation of amount.

MyNumber = Trim(Str(MyNumber))

' Position of decimal place 0 if none.

DecimalPlace = InStr(MyNumber, ".")

' Convert fils and set MyNumber to dirham amount.

If DecimalPlace > 0 Then

Fils = GetTens(Left(Mid(MyNumber, DecimalPlace + 1) & "00", 2))

MyNumber = Trim(Left(MyNumber, DecimalPlace - 1))

End If

Count = 1

Do While MyNumber <> ""

Temp = GetHundreds(Right(MyNumber, 3))

If Temp <> "" Then Dirhams = Temp & Place(Count) & Dirhams

If Len(MyNumber) > 3 Then

MyNumber = Left(MyNumber, Len(MyNumber) - 3)

Else

MyNumber = ""

End If

Count = Count + 1

Loop

Select Case Dirhams

Case ""

Dirhams = "No Dirhams"

Case "One"

Dirhams = "One Dirham"

Case Else

Dirhams = Dirhams & " Dirhams"

End Select

Select Case Fils

Case ""

Fils = " and No Fils"

Case "One"

Fils = " and One Fil"

Case Else

Fils = " and " & Fils & " Fils"

End Select

SpellNumber = Dirhams & Fils

End Function

' Converts a number from 100-999 into text

Function GetHundreds(ByVal MyNumber)

Dim Result As String

If Val(MyNumber) = 0 Then Exit Function

MyNumber = Right("000" & MyNumber, 3)

' Convert the hundreds place.

If Mid(MyNumber, 1, 1) <> "0" Then

Result = GetDigit(Mid(MyNumber, 1, 1)) & " Hundred "

End If

' Convert the tens and ones place.

If Mid(MyNumber, 2, 1) <> "0" Then

Result = Result & GetTens(Mid(MyNumber, 2))

Else

Result = Result & GetDigit(Mid(MyNumber, 3))

End If

GetHundreds = Result

End Function

' Converts a number from 10 to 99 into text.

Function GetTens(TensText)

Dim Result As String

Result = "" ' Null out the temporary function value.

If Val(Left(TensText, 1)) = 1 Then ' If value between 10-19...

Select Case Val(TensText)

Case 10: Result = "Ten"

Case 11: Result = "Eleven"

Case 12: Result = "Twelve"

Case 13: Result = "Thirteen"

Case 14: Result = "Fourteen"

Case 15: Result = "Fifteen"

Case 16: Result = "Sixteen"

Case 17: Result = "Seventeen"

Case 18: Result = "Eighteen"

Case 19: Result = "Nineteen"

Case Else

End Select

Else ' If value between 20-99...

Select Case Val(Left(TensText, 1))

Case 2: Result = "Twenty "

Case 3: Result = "Thirty "

Case 4: Result = "Forty "

Case 5: Result = "Fifty "

Case 6: Result = "Sixty "

Case 7: Result = "Seventy "

Case 8: Result = "Eighty "

Case 9: Result = "Ninety "

Case Else

End Select

Result = Result & GetDigit(Right(TensText, 1)) ' Retrieve ones place.

End If

GetTens = Result

End Function

' Converts a number from 1 to 9 into text.

Function GetDigit(Digit)

Select Case Val(Digit)

Case 1: GetDigit = "One"

Case 2: GetDigit = "Two"

Case 3: GetDigit = "Three"

Case 4: GetDigit = "Four"

Case 5: GetDigit = "Five"

Case 6: GetDigit = "Six"

Case 7: GetDigit = "Seven"

Case 8: GetDigit = "Eight"

Case 9: GetDigit = "Nine"

Case Else: GetDigit = ""

End Select

End Function

Financial reporting consolidation is the process of combining financial data from various business units or subsidiaries within an organization to produce a consolidated set of financial statements. This process involves collecting, validating, and aggregating financial information from various sources to provide a comprehensive view of an organization’s financial position, performance, and cash flow.

The process of financial statement consolidation includes the following steps:

Collection of financial data: This includes collecting financial data from various sources such as sub-financial statements, general ledger, balance sheet, bank statement, etc.

Reconciliation of intragroup transactions: Where multiple business units or subsidiaries are involved, there may be intercompany transactions that need to be eliminated or adjusted to avoid double counting revenues and expenses.

Elimination of minority shareholders: If the parent company does not own 100% of the subsidiary’s shares, the portion of the subsidiary’s results belonging to minority shareholders is excluded from the consolidated financial statements. Currency conversion: If subsidiaries operate in different countries with different currencies, their financial data must be converted into a common currency for consolidation purposes.

Create a delete entry: A deletion posting is made to remove all intercompany transactions and balances adjusted in step 2.

Consolidated financial statements: After all customizations are complete, consolidate your financial statements to create a single set of financial statements for your entire organization.

Analysis of Consolidated Financial Statements: The final step is to analyze the consolidated financial statements to assess the organization’s overall financial performance.

In summary, the process of consolidating financial reporting involves combining financial data from various business units or subsidiaries to obtain a comprehensive view of an organization’s financial position, performance, and cash flow. This process is critical to providing stakeholders with accurate and reliable information for decision-making and compliance purposes.

To avoid repeated postings during consolidation, it is important to conduct a thorough review and analysis of the financial data being consolidated. Here are some steps you can take to prevent repeated entries:

Create an integration plan. Before you consolidate your financial statements, it is important to develop a consolidation plan that outlines the steps you will take to avoid duplicate entries. This plan should include reviewing the chart of accounts, reviewing intercompany transactions, and reviewing other areas where duplicate entries may occur.

Check your chart of accounts. One of the first steps to verify your entries is to check your chart of accounts. This allows you to identify duplicate or misclassified accounts. This review should include a comparison of the chart of accounts of each consolidated subsidiary or entity to ensure that there are no duplicates.

Check intercompany transactions. Intercompany transactions can be a significant source of duplicate entries. These transactions occur when a subsidiary or business unit within an organization transacts with another subsidiary or business unit. It is important to review intercompany transactions to ensure they are properly recorded and duplicate entries are removed.

Use integrated software. Consolidation software automates the consolidation process and helps identify duplicate entries. The software flags potential duplicate entries for quick and efficient review and elimination.

Do a detailed check. Finally, it is important to conduct a detailed review of consolidated financial data. This review should include a general ledger comparison for each consolidated subsidiary or business unit and a review of all other financial data such as: B. Includes balance sheet and bank statement. A full scan allows you to identify potential duplicate entries and take action to eliminate them.

Overall, avoiding repeated postings during consolidation requires careful planning and review of financial data. Following these procedures will help ensure the accuracy and reliability of our consolidated financial statements.

The International Chamber of Commerce (ICC) has published the Uniform Customs and Practice for Documentary Credits (UCP 600) as a set of guidelines for banks and businesses engaged in international trade. Some of the key provisions of UCP 600 include:

General provisions: The UCP 600 outlines the general principles that govern the use of documentary credits in international trade, including the obligation of banks to act in accordance with the terms and conditions of the credit, and the requirement that all documents be presented within a specified time frame.

Obligations and liabilities: The UCP 600 sets out the obligations and liabilities of the various parties involved in a documentary credit transaction, including the buyer, seller, issuing bank, and advising bank.

Examination of documents: The UCP 600 provides guidelines for the examination of documents by banks, including the requirement that all documents be examined within a reasonable time frame, and that banks may only reject documents that do not comply with the terms and conditions of the credit.

Discrepancies and waivers: The UCP 600 provides guidelines for dealing with discrepancies in documents, including the requirement that banks must notify the buyer and seller of any discrepancies, and the procedures for obtaining waivers or amendments to the credit.

Transferable credits: The UCP 600 outlines the rules and procedures for transferring a documentary credit to a third party.

Confirmation: The UCP 600 provides guidelines for confirming banks, including the requirements for a confirming bank to undertake to pay, accept or negotiate documents under the credit.

Electronic documents: The UCP 600 recognizes the use of electronic documents in documentary credit transactions and sets out guidelines for the use of electronic documents, including the requirements for electronic signatures and the use of secure messaging systems.

Availability of funds: The UCP 600 sets out the rules and procedures for the availability of funds under a documentary credit, including the requirement that banks may only pay or negotiate documents if funds are available.

International Standard Banking Practice (ISBP 745) is a set of guidelines established by the International Chamber of Commerce (ICC) to provide guidance on the interpretation of the Uniform Customs and Practice for Documentary Credits (UCP 600) in the context of documentary credit transactions. Following the ISBP 745 guidelines is important for LC payment requests for several reasons:

Facilitate document examination: The ISBP 745 guidelines provide guidance on the examination of documents by banks, including the standards for document preparation, the acceptance of electronic documents, and the handling of discrepancies. By following these guidelines, parties involved in LC transactions can facilitate the examination of documents by banks, which can help to speed up the payment process.

Reduce costs and delays: By following the ISBP 745 guidelines, parties involved in LC transactions can reduce the risk of discrepancies and delays in the payment process. This can help to reduce costs associated with delays and additional document preparation, and improve the efficiency of the payment process.

Image Credit: Google Images

Improve communication and understanding: The ISBP 745 guidelines help to improve communication and understanding between the parties involved in LC transactions. By following these guidelines, parties can ensure a common understanding of the requirements for LC transactions, and reduce the risk of misunderstandings or disputes.

In summary, following the ISBP 745 guidelines is important for LC payment requests because it helps to ensure compliance with the UCP 600, reduce discrepancies, facilitate document examination, reduce costs and delays, and improve communication and understanding between the parties involved in LC transactions.

“LC” typically stands for “Letter of Credit.” A Letter of Credit is a document issued by a bank that guarantees payment to a seller for goods or services, provided that certain conditions are met. Essentially, the bank acts as an intermediary between the buyer and the seller, ensuring that the seller will receive payment if they fulfill the terms of the Letter of Credit.

LC discounting, also known as “LC financing,” is a process in which a seller obtains cash from a bank or financial institution by selling their Letter of Credit at a discount. This allows the seller to receive payment for their goods or services more quickly than they would if they had to wait for the buyer to pay the bank directly.

How to understand it in practical situation?

In a practical situation, LC discounting may be used in international trade when the seller needs access to cash before the buyer has paid for the goods or services. The seller can sell the Letter of Credit to a bank or financial institution at a discount, and receive cash immediately. The bank then assumes the risk that the buyer will not pay, and takes on the responsibility of collecting payment from the buyer when it is due.

To do LC discounting in a practical situation, the seller would typically need to find a bank or financial institution that is willing to purchase their Letter of Credit at a discount. The discount rate would depend on factors such as the creditworthiness of the buyer and the terms of the Letter of Credit. The bank or financial institution would then provide the seller with the cash they need and assume the risk of collecting payment from the buyer at a later date.